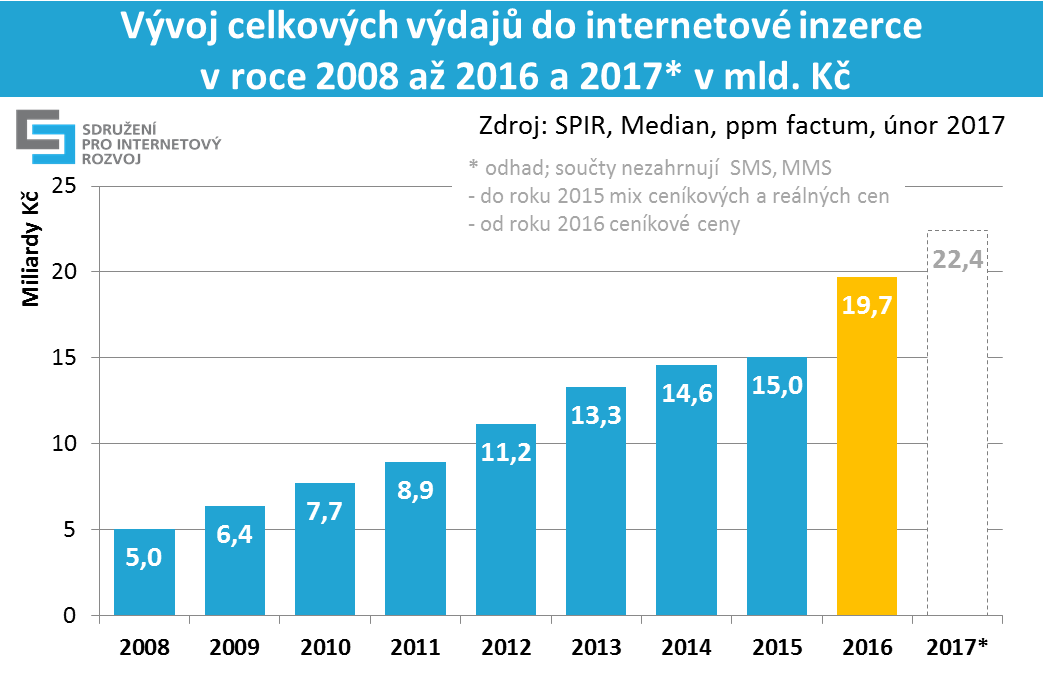

Prague, March, 8 2017 – Last year the volume of internet advertising reached almost CZK 20 billion in ratecard prices. Compared to 2015, this represents a 31 per cent growth that was caused primarily by increased advertising expenditures in search advertising, content networks and RTB. Expectations for the coming year are also optimistic; the survey participants assume that online advertising will continue to grow by 14 per cent up to CZK 22, 4 billion in 2017. Out of the total advertising expenditures across all media types, online advertising accounts for a 21 per cent share. The data come from the annual survey of Internet advertising performance conducted for SPIR by Median.

In 2016 advertisers used online advertising in the volume of CZK 19,7 billion, which is by 31 per cent more than in the previous year. “This year has confirmed the ongoing growing trend in the use of online forms of advertising. The Czech Republic ranks amongst countries, where the internet is the second most significant media type,” comments Ján Simkanič, the SPIR Chairman.

Development of Total Expenditures in Internet Advertising in the Period of 2008-2016 and 2017*, in billion CZK

chart 1: The Development of Total Expenditures in Internet Advertising

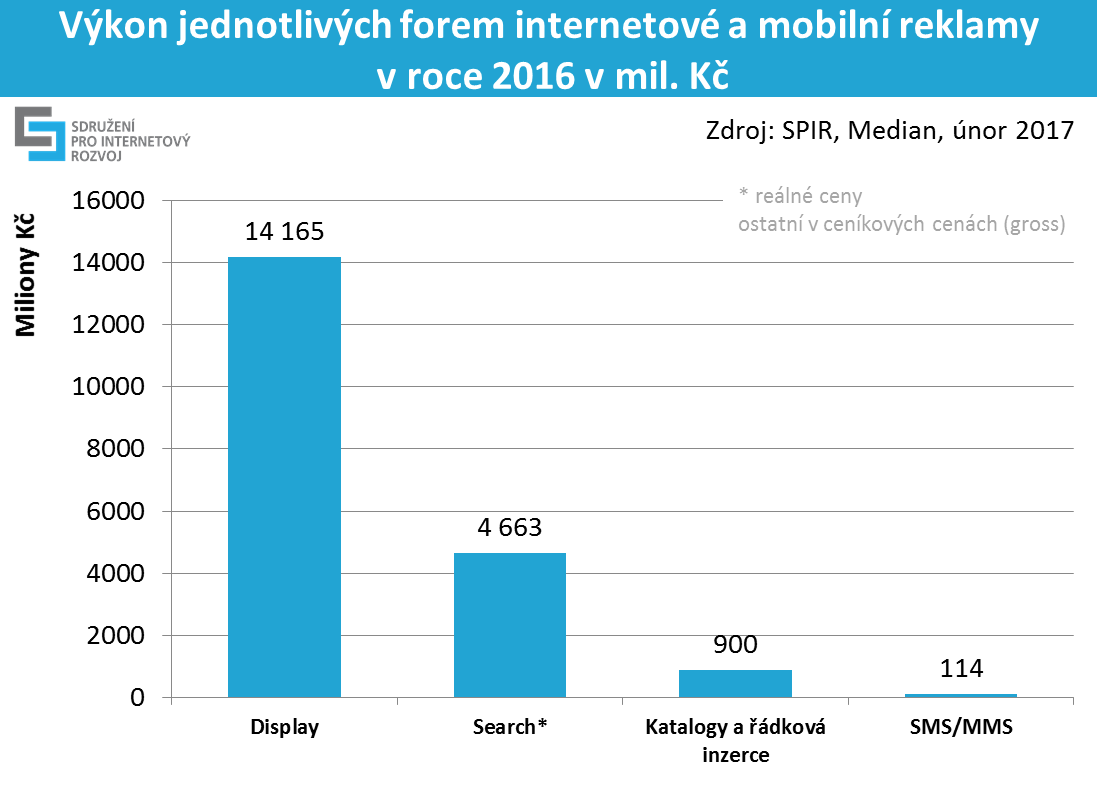

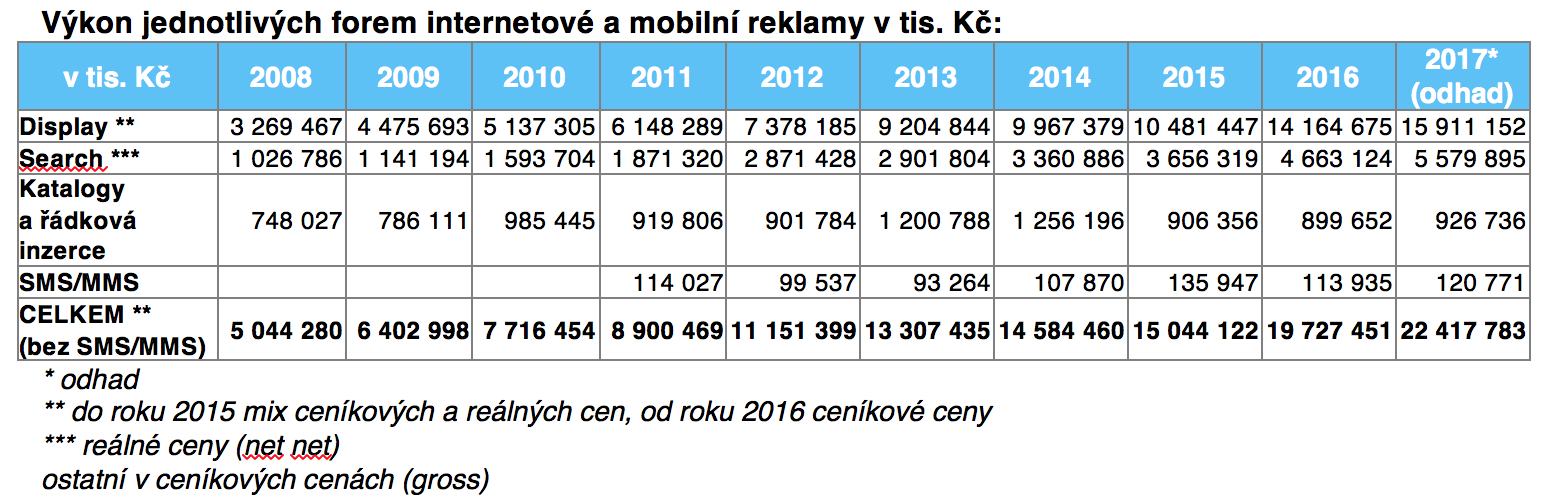

The largest part of advertising expenditures is attributable to display advertising (CZK 14,2 billion). This year a new output structure has been used; as opposed to last years, the display advertising includes also advertising in content networks (in particular Seznam Sklik, Google AdWords and Facebook), RTB and native advertising. The second most frequently used advertising form is paid search with expenditures of CZK 4,7 billion in real prices. The sales in respect of classifieds and directories were declared in the amount of CZK 900 million in ratecard prices. With respect to SMS and MMS campaigns, which are not being included in internet advertising, the advertisers spent CZK 114 million in ratecard prices.

This year for the first time the performance of video advertising may be determined in a more precise manner; its share within the overall display advertising was 19 % (CZK 2,75 billion. Native advertising had almost a one per cent share (CZK 80 million).

chart 2: Market share of Individual Internet Advertising Forms in 2016

Another new feature of the survey is the possibility to determine the share of mobile advertising not only with respect to standard display, as declared by media, but also in relation to content networks and RTB. The share of mobile advertising out of the overall display advertising was 12 per cent (CZK 1,75 billion).

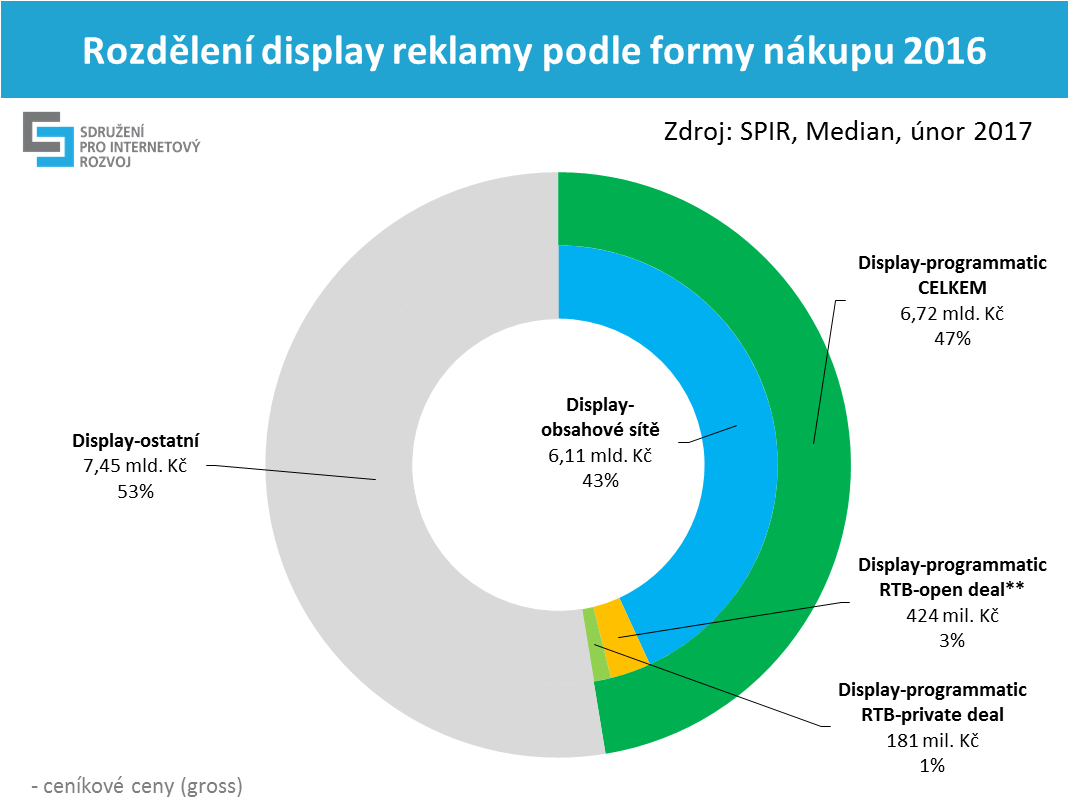

chart 3: Breakdown of display advertising according to the purchase form in 2016

The programmatic business model is becoming more and more important and therefore the manner of display advertising purchase is also reflected. Out of the total advertising expenditures the programmatic forms have a one third share (34 per cent). Programmatic forms of advertising include content networks and RTB, which together represented a 47 per cent share (CZK 6,72 billion in ratecard prices). Content network reached a 43 per cent share (CZK 6,11 billion in ratecard prices), while RTB represented a 4 per cent share (CZK 605 million in ratecard prices).

With respect to programmatic advertising, which in 2016 reached the volume CZK 5,84 billion in real prices, the highest share (91 per cent) was represented by content networks (CZK 5,31 billion in real prices). RTB share was 9 per cent with the total volume of CZK 526 million in real prices.

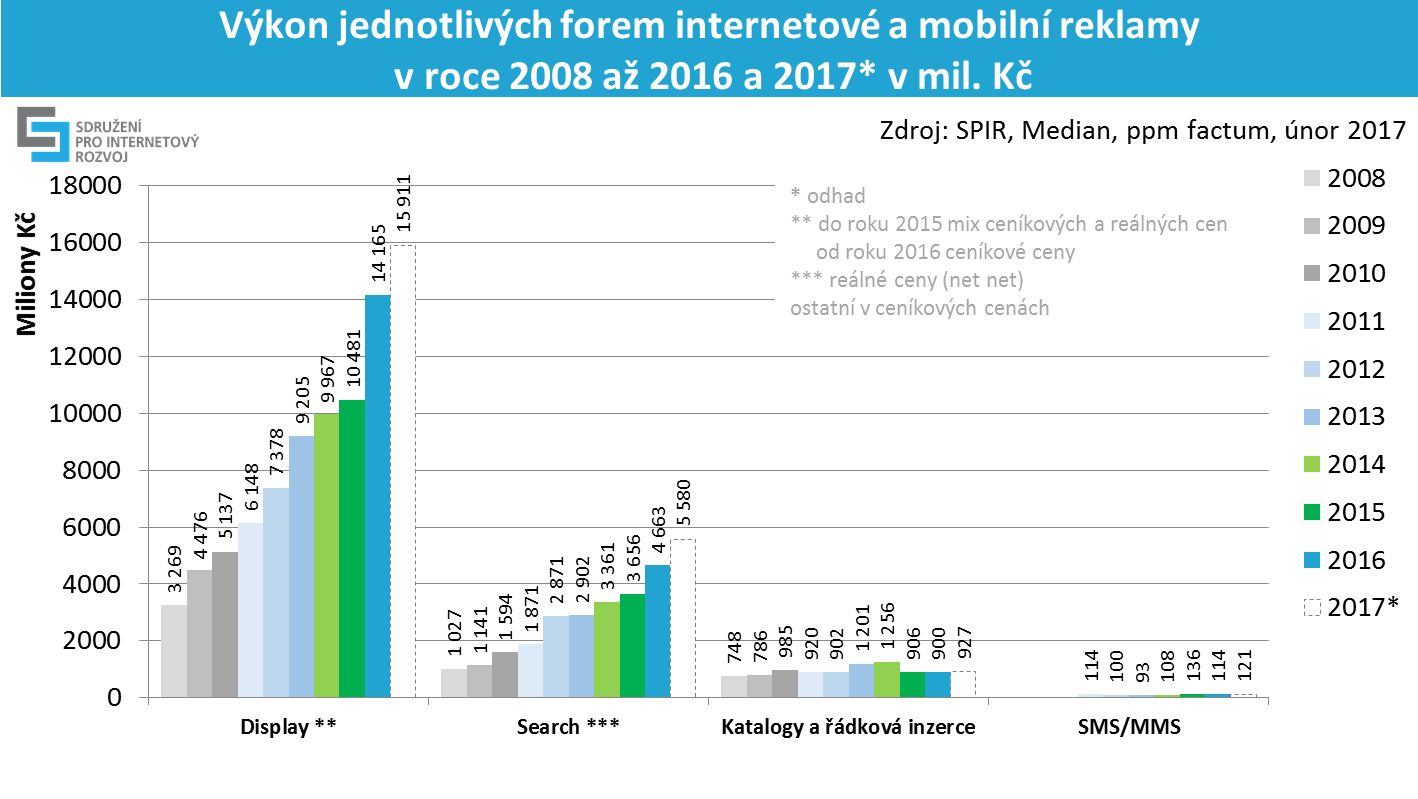

Development of Individual Forms of Internet and Mobile Advertising in the Period of 2008-2016 and 2017*

This year the structure of results differs and therefore the figures covering past years had to be adjusted to a comparable structure in order to follow development of individual forms within a longer timeline. The long-term growth is clearly visible in the case of display and search advertising. As far as the display advertising is concerned, the growth is caused primarily by programmatic forms – content networks and RTB – that were calculated from real to ratecard prices in the amount of + 15 per cent)[1].

chart 4: Performance of individual forms of internet advertising in the period of 2008-2016 and 2017

table 1: Performance of individual forms of internet and mobile advertising in CZK ths

Share of Individual Mediatypes in 2016

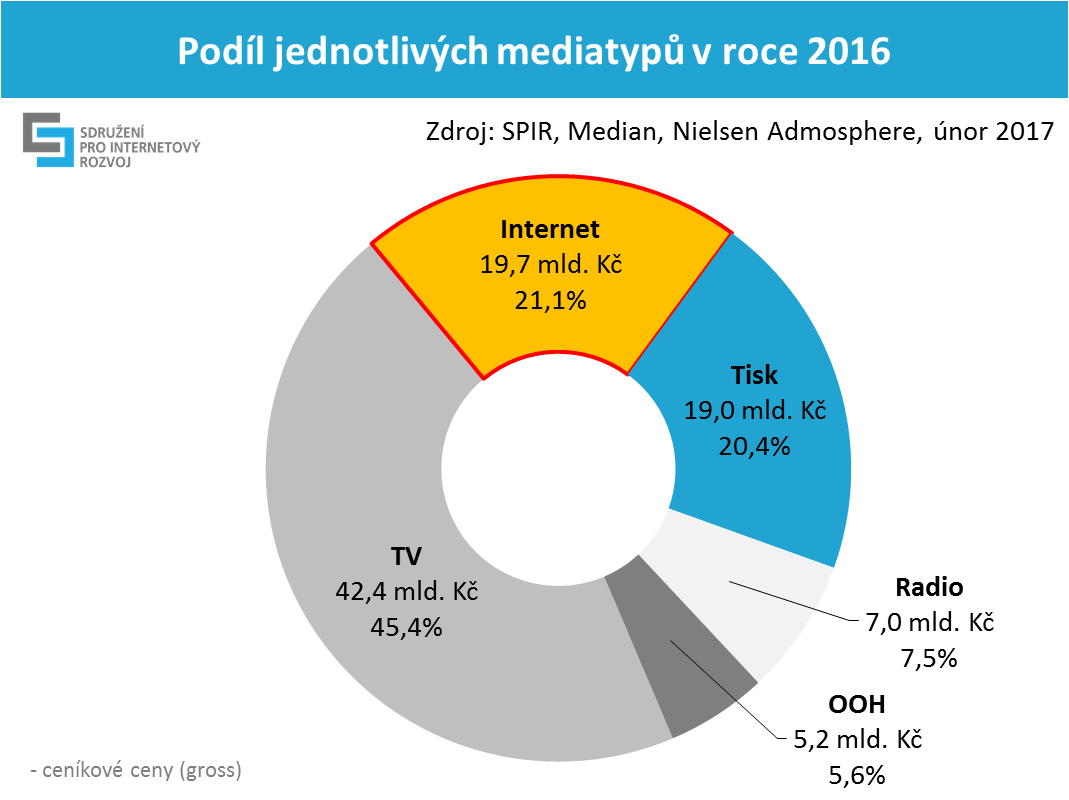

For the purpose of comparing the volume of advertising in individual media types, data derived from the Nielsen Admosphere monitoring of advertising expenditures were used. TV advertising with CZK 42,4 billion maintains its dominant position in the advertising market (45 per cent). Online advertising has a 21 per cent share (CZK 19,7 billion). Press advertising reached CZK 19 billion and has a 20 per cent share in advertisement budgets. Radio advertising reached the level of CZK 7 billion (8 per cent) and OOH advertising generated CZK 5,2 billion (6 per cent) last year. The prices do not include self-promotion. Since 2008, when the SPIR online advertising performance survey started, we note a long-term growing trend of expenditures in internet advertising.

chart 5: Individual Mediatype Share in 2016

The full version of the internet advertising performance is to be found at http://www.inzertnivykony.cz.

The used types of internet advertising are to be found at http://www.inzertnivykony.cz/terminologie-metodika.

More detailed description of advertising forms are to be found at http://www.spir.cz/reklamni-formaty-a-html-5.

Below you will find selected terms that might be incorrectly understood from the viewpoint of terminology. A more detailed version is to be found at the above specified links.

Internet display advertising: Banner advertising in standard (banners, skyscrapers, leaderboards...) and non-standard formats (overlays, interstitials) and video banners. Now the display advertising also includes content network and RTB.

Paid search advertising: Advertising appearing on specific word requests on search engines or premium positions.

Programmatic: automated process of purchase and sale of digital advertising space. Display programmatic includes content network and RTB.

RTB (real-time-bidding) is a type of business model for selling banner advertising targeted at desired audience, where each impression is delivered in real time by automatic systems as is appropriate for the required target group. In the RTB model, geographical, linguistic or behavioural targeting of advertising is often used, on the basis of previous activity and the interests of the user. The main characteristic of the RTB model is the auction sale in real prices of advertising. Now RTB advertising is included within display advertising.

Methodology Description

For the purpose of surveying and processing the results, in the interest of objectivity and the protection of sensitive data, the Median agency was commissioned. The survey was conducted during January and February 2017 and was based on current closings of individual subjects. The performance of all types of advertising was based on declared performance of individual providers of content, agencies, and operators of advertising networks and mobile operators.

From the important internet operators, who were addressed, 21 became actively involved; their media have impact on vast majority of Czech Internet users. In case of 4 operators, who did not submit the results, data of AdMonitoring survey was used. All 3 addressed mobile operators provided financial data related to SMS and MMS advertising messages. In order to obtain data on the performance of individual advertising networks, three operators, 60 media, digital and specialized agencies, as well as 182 direct advertisers were addressed. To calculate the total advertised amount in advertising networks, the claimed performance of the Sklik advertising network is used; along with the percentage distribution of spending by agencies into advertising networks . Breakdown of performance into search and content networks is based on declared data by agencies and direct advertisers. For the first time operators of DSP systems were addressed in order to calculate the overall RTB programmatic advertising through shares of individual DSP with respect of agencies and direct advertisers. Taking into consideration the low participation of DSP operators the calculation was not possible, or better to say, it would be subject to significant statistical mistake. The RTB volume was thus determined as a sum of declared performance by agencies and direct advertisers.

This year, for the first time, partial correction was made in terms of the display advertising forms that are obtained in real (net net) prices and lack ratecard prices. For the purpose of better comparison with the volume of other advertising, which is indicated in ratecard prices, as well as other media types, the prices of programmatic forms (content networks and RTB) were increased by 15 per cent, which may be regarded as the basic charge. The difference between a ratecard and real price is, undoubtedly, higher but because of insufficient support the minimal value was finally used. Our objective in further years of the survey is to quantify the difference more precisely.

For the purpose of transparency, volumes of programmatic forms of display advertising are indicated in real (net net) prices. Search advertising remains in real prices, and since it is not display advertising, the subsequent calculation is not necessary. The remaining media types use ratecard prices; estimates of real prices are not available. The overall performance of the internet does not include SMS and MMS campaigns, which cannot be considered as a type of internet advertising.

For more details, please, contact:

Peter Kokavec – technical inquiries

SPIR Project Manager

mobile: 775 200 949

e-mail: [email protected]

Petr Kolář – technical inquiries

Analyst

mobile: 603 749 847

e-mail: [email protected]

Tereza Tůmová – other inquiries

PR Manager

mobile: +420 739 465 233

e-mail: [email protected]

[1] For more details on the calculation see Methodology.